Introduction

Welcome to a comprehensive guide on the taxation of companies in the Netherlands. In this article, we will explore the key aspects of corporate taxes in one of the world’s most business-friendly countries. Whether you are a multinational corporation or a small startup, understanding the tax system is essential for optimizing your financial operations.

The Netherlands is known for its favorable tax policies and attractive tax incentives. With relatively low corporate tax rates and various deductions available, the country encourages companies to thrive and invest in innovation. Moreover, its extensive network of double tax treaties ensures favorable tax treatment for businesses with international operations.

In this guide, we will delve into the fundamentals of corporate taxation in the Netherlands, including the corporate tax rate, tax brackets, deductions, and exemptions. We will also discuss special tax regimes for specific types of companies, such as the Innovation Box and the Fiscal Investment Institution.

So, if you are looking to establish or expand your business in the Netherlands, join us as we navigate the intricacies of the country’s corporate tax regime and unlock valuable tax advantages for your company. Let’s dive in!

Types Of Taxes Applicable To Companies In The Netherlands

When operating a business in the Netherlands, it is crucial to understand the various types of taxes that may apply to your company. The primary taxes that companies need to consider are corporate income tax, value-added tax (VAT), and withholding tax.

Corporate Income Tax In The Netherlands

Corporate income tax is levied on the profits generated by companies in the Netherlands. The corporate tax rate in the Netherlands is currently set at 25%. However, for profits up to €200,000, a reduced tax rate of 15% applies. This lower rate aims to support small and medium-sized enterprises (SMEs) and stimulate entrepreneurial activities.

In addition to the corporate tax rate, companies are also subject to municipal taxes, which vary depending on the location of the business. It is important to note that the Netherlands operates on a territorial tax system, meaning that only profits derived from Dutch sources are subject to taxation.

Value Added Tax (VAT) In The Netherlands

Value Added Tax, commonly known as VAT, is a consumption tax levied on the sale of goods and services. In the Netherlands, the standard VAT rate is 21%. However, there are reduced VAT rates of 9% and 0% applicable to specific goods and services.

The 9% reduced rate is primarily applied to essential items such as food, books, and cultural events. On the other hand, certain goods and services, such as exports and international transport, are zero-rated, meaning no VAT is charged. VAT registration is mandatory for companies in the Netherlands once their turnover exceeds the threshold of €20,000.

Withholding Tax In The Netherlands

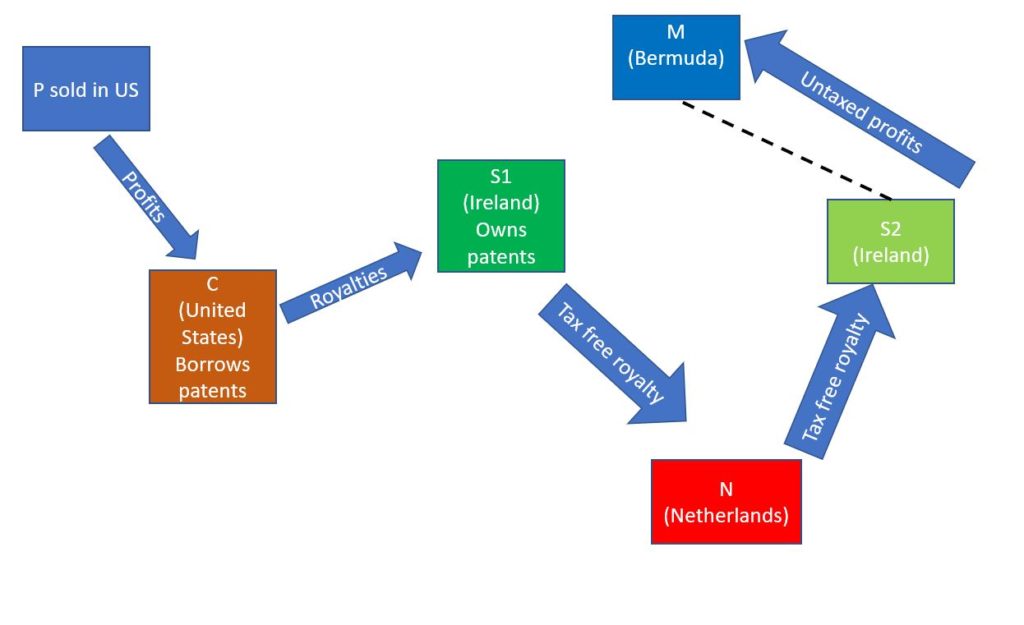

Withholding tax, also known as retention tax, is a tax deducted at the source of payments made to non-residents. In the Netherlands, withholding tax is typically applied to dividends, interest, and royalties paid to foreign entities. However, the country has an extensive network of double tax treaties, which often reduce or eliminate withholding tax for residents of treaty countries.

The Netherlands also offers participation exemption, which allows companies to receive dividends from subsidiaries without being subject to withholding tax. This exemption aims to promote international business activities and encourage the use of Dutch holding companies.

Tax Incentives And Exemptions For Businesses In The Netherlands

To attract investment and stimulate economic growth, the Netherlands offers various tax incentives and exemptions for businesses. These incentives aim to reduce the overall tax burden and encourage companies to innovate and expand their operations.

Innovation Box

The Innovation Box is a special tax regime that provides a reduced corporate tax rate of 7% on profits derived from qualifying intellectual property (IP). This regime aims to promote research and development activities in the Netherlands and encourage companies to create and exploit innovative products, services, and technologies.

To be eligible for the Innovation Box, companies need to meet specific criteria regarding the development and ownership of IP. By opting for this regime, businesses can significantly reduce their tax liability on income derived from qualifying intangible assets.

Fiscal Investment Institution (FII)

The Fiscal Investment Institution (FII) is a tax regime designed to attract investment in certain sectors, such as real estate and infrastructure. Under this regime, qualifying investments are exempt from corporate income tax and dividend withholding tax. The FII regime aims to stimulate investment in sectors that contribute to the Dutch economy and create jobs.

To qualify for the FII regime, companies need to meet specific requirements, such as investing in qualifying assets and distributing a minimum percentage of the profits to shareholders.

Double Tax Treaties And Their Impact On Dutch Companies

The Netherlands has an extensive network of double tax treaties with countries around the world. These treaties aim to prevent double taxation and provide favorable tax treatment for businesses with international operations.

Under a double tax treaty, companies can benefit from reduced withholding tax rates, exemption or credit for foreign taxes paid, and protection against discriminatory tax measures. These treaties also provide certainty and clarity on the taxation of cross-border transactions and help avoid potential disputes between countries.

For Dutch companies with global operations, double tax treaties play a crucial role in minimizing tax liabilities and optimizing international tax planning strategies.

Compliance And Reporting Requirements For Dutch Companies

Like any other jurisdiction, the Netherlands has specific compliance and reporting requirements that companies need to adhere to. It is essential to maintain accurate and up-to-date financial records, prepare annual financial statements, and file tax returns within the prescribed deadlines.

Dutch companies are also obliged to comply with transfer pricing regulations to ensure that transactions between related entities are conducted at arm’s length. Transfer pricing documentation is required to demonstrate that intercompany transactions are priced in line with market conditions.

Failure to comply with these obligations may result in penalties, interest charges, and potential reputational damage for the company.

Common Tax Planning Strategies For Companies In The Netherlands

To optimize their tax position, companies in the Netherlands often employ various tax planning strategies. These strategies aim to minimize tax liabilities while remaining compliant with applicable laws and regulations.

Some commonly used tax planning strategies include:

Group Financing Structures: By establishing a group financing company in the Netherlands, companies can benefit from favorable tax treatment on interest payments, such as the deduction of interest expenses.

R&D Tax Credits: The Netherlands offers generous tax credits for research and development (R&D) activities. By properly documenting and claiming eligible R&D expenses, companies can reduce their tax liabilities and stimulate innovation.

Intellectual Property Planning: Companies with valuable intellectual property often employ tax-efficient strategies to maximize the return on their IP. This may involve the use of licensing agreements, cost-sharing arrangements, and the application of the Innovation Box regime.

Transfer Pricing Optimization: Ensuring that intercompany transactions are priced in line with market conditions is essential for minimizing tax risks. Companies need to establish robust transfer pricing policies and documentation to support their pricing decisions.

Conclusion

The Netherlands offers an attractive tax environment for companies, with relatively low corporate tax rates, favorable tax incentives, and an extensive network of double tax treaties. Understanding the taxation of companies in the Netherlands is crucial for optimizing tax planning strategies and maximizing tax advantages.

By familiarizing yourself with the corporate tax rate, types of taxes applicable, exemptions, and tax planning opportunities, you can make informed decisions to enhance your company’s financial position. However, it is essential to consult with tax professionals who specialize in Dutch tax law to ensure compliance and optimize tax planning strategies tailored to your specific circumstances.

Remember, tax laws and regulations are subject to change, so it is crucial to stay updated and adapt your tax strategies accordingly. With careful planning and expert guidance, your company can benefit from the Netherlands’ business-friendly tax system and unlock valuable tax advantages.